The Great Australian Labour Crisis

Something's gotta give, so who will win and who will lose?

South East Queensland is looking down the barrel of a very strange decade.

I believe that things are going to get bumpy. If I were a flight attendant, I would turn on the fasten seatbelt light.

Consider the following 4 ingredients:

Ingredient 1: The present day housing crisis

Australia is currently in the throes of a worsening housing crisis, with no signs of slowing. Some headlines:

122,494 people are experiencing homelessness, with 1,600 people being pushed into homelessness each month.

An estimated 424 homeless people die on the street every year.

Australia has somewhere between the third and sixth highest rate of homelessness in the OECD as a percentage of the population.

The national shortage of social and affordable homes is 640,000 and is expected to grow over 75,000 over the next five years as the crisis deepens. Based on projected household growth, there will be over 940,000 households in 2041 with unmet housing needs.

In Queensland alone, 45,958 people are on the social housing waitlist, with 27,438 of those assessed as high needs. Meanwhile, social housing built by the Queensland Government per year numbers in the hundreds - which barely keeps pace with demolitions and sales.

377,600 households are in housing need, or 33,100 in rental stress and 46,500 experiencing homelessness.

It will take the average Australian 11.4 years to save a 20% deposit for an average Australian home (a record high).

Despite skyrocketing rents, Brisbane’s rental vacancy rate has remained persistently at historically low levels of 0.90%. (while a healthy vacancy rate is considered to be 2.6% - 3.5%).

Meanwhile, we are building the world’s biggest houses.

Most of those aren’t even projections, that’s just how things are right now.

Ingredient 2: Population growth

What’s good for a housing crisis? More people of course! The recently released South East Queensland Regional Plan Update sets the stage for a generation of significant population growth, enabled by high levels of interstate and overseas migration and an ambitious urban renewal agenda.

Some headlines:

2.2 million new residents and 863,000 new dwellings in South East Queensland by 2046.

209,700 of the above are to be delivered in the Brisbane LGA, of which approximately 60% is planned to be urban infill renewal (significantly slower, more complex and costly).

Queensland needs to deliver 34,700 new dwellings per year to meet the above rate.

Queensland and Brisbane have consistently maintained the highest rate of net interstate migration in the country in recent years.

Net overseas migration is slated to be 268,000 higher than expected for the 2022-2025 period.

Ingredient 3: Slowing construction activity

The inflation and high interest rates of recent years has led to massive increases in labour and material costs, causing hundreds of builders across the country to go insolvent. So despite all this dire demand for housing, construction activity is actually slowing down.

Some headlines:

Earlier than expected increases in interest rates has slowed the national outlook for new supply, from 148,500 in 2022-2023, down to 127,500 in 2024-2025.

Brisbane currently has the highest construction labour cost in the country.

QLD tops the nation with a 14.4% increase in construction costs in 2022.

Tender prices have increased 5.1% in Brisbane, and 10.5% on the Gold Coast.

1,086 construction businesses have gone insolvent from January to May in Queensland alone, accounting 26% of business insolvencies across Australia during the same period.

There is currently a shortage of 8,500 of construction workers per month in Queensland, with this anticipated to grow.

25-30% of developments across Australian capital cities do not have a builder organised.

Dwelling approvals are at their lowest since 2012.

Total dwelling commencements fell by 21.2% for the year up to the September 2022 quarter.

International freight costs have increased 7-8 times over previous levels.

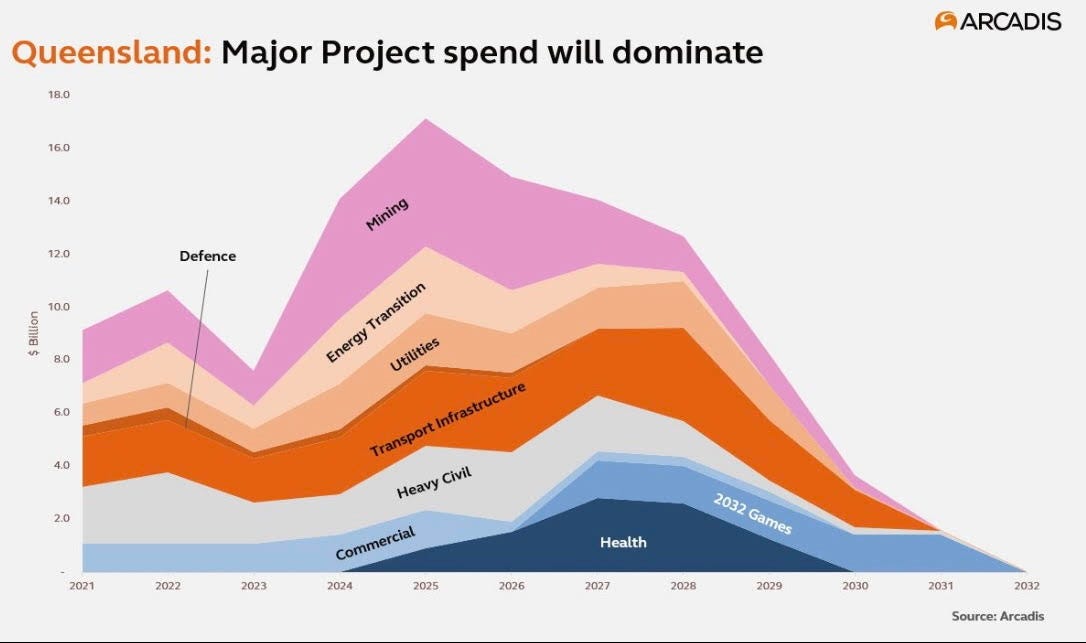

Ingredient 4: A Historic Pipeline of Major Projects

But wait, there’s more.

Amidst all of this tension, Queensland is gearing up for a historic period of public and private infrastructure spending, with $71.3 billion slated for Queensland and $56 billion slated for South East Queensland alone.

Let’s go down the list:

(At least) $7 billion in spending on the Brisbane 2032 Olympic Games.

$10 billion on health projects.

$12.6 billion in rail and harbours projects.

$12.9 billion in roads and bridges projects.

$23.2 billion in mining and heavy industry projects.

$1.4 billion in defence projects.

$5.9 billion in water and sewerage infrastructure projects.

$2.1 billion in education projects.

All of the above big, complex, expensive and long-running projects are being planned, procured, designed and delivered in the 8-9 years leading up to the 2032 Olympics.

It all comes together in the perfect storm

So we’re in this situation where the present day housing crisis, exacerbated by population growth is driving up demand for new housing. Yet in our time of need, construction activity is actually slowing, due to high costs, high interest rates and general uncertainty.

As if that wasn’t bad enough, these trends are converging on an era of historic infrastructure spending and the lead up to the 2032 Olympics - a period where we will presumably need significantly more labour than normal.

Ok, but what does that actually mean?

The Great Australian Labour Crisis

Competition for construction labour during this period could create an extremely volatile environment for delivering housing and the above projects - driving up costs further still.

This will presumably exacerbate the housing crisis and drive more people into homelessness, all in the lead up to the highly-visible 2032 Olympics - where I’m sure we would all prefer there to be significantly less homelessness.

We may be inevitably be faced with a choice - cancel certain projects, or import the labour. If we choose the latter, where are they going to live?

Until someone comes up with something better, I am calling this The Great Australian Labour Crisis - where it is on for young and old in the scramble for construction labour and adjacent professional services.

Loyalties will be tested. Standards will be lowered. DIYs will be... attempted. Fathers will turn against sons. Cousins against uncles. Every tradie will have 7 jetskis. Ice break sales will skyrocket.

In this environment of great instability, only one thing is certain, Tim Gurner will not be happy.

Am I wrong?

As always, I am a strictly vibes-based economist (i.e. not an economist at all), and am acutely aware of my tendency to freak myself out by assembling horrible statistics - unfortunately how my brain works.

If I’m wrong, please tell me so and I will amend this article to be more uplifting.

Subscribe to my Substack!

As a subscriber, you’ll get my full articles (complete with images) in your email inbox - sparing you having to go to the actual website or be lucky enough to spot my articles in your feed. For whatever reason I find this a much more enjoyable and consistent way to read the writers I follow, so if you have enjoyed any of my articles so far, please subscribe.

Yes, many thanks. I have been eagerly awaiting your post.

Clarify please: 'Queensland and Brisbane have consistently maintained the highest rate of net interstate migration in the country in recent years.' I presume you mean immigration. Migration could imply a loss of people.

What are the complexities involved in urban infil?

How much more does urban infil cost per square metre of finished house by comparison with a house in the greenfield extremity. Tim Gurner probably knows.

What proportion of urban infil occurs in residential areas or is it normally on brownfield sites or government land? Would a developer ever consider amalgamating titles and re-arranging the road network?

Do you see instances of developers building communities that have a liberal approach to zoning so as to enable people to obtain what they require within walking distance?

What would the population potential in the largest infill project? My thinking is that unless its large there will be little scope to change the zoning scheme so as to maximize the potential to build in everyday interactions between people to mitigate the loneliness experienced in single use Aussie urban sprawl.

I note the new planning initiatives in Melbourne to incentivize developers to get involved in infil projects in return for fast tracking approvals via the Minister for planning rather than face the delays involved in the current planning arrangements. But I really wonder whether this will create places that are favorable to interpersonal interactions required to develop a community of interdependent people who enjoy the support of each other.

It's one thing to be able to build, it's another thing entirety to build something worth having. In my view it is going to be easier and cheaper to satisfy needs on a greenfield site with a deliberately liberal approach to zoning. To appreciate the potential, simply make a list of the occupations that could be pursued if we allowed people to design a house that incorporated a workshop, a retail outlet and a residence combined, all of which have the potential to be rented as accommodation if a person decides to retire. Don't be aghast at this possibility because this is what people do in rural villages.

Perhaps we could rebuild our community from the single household up. Re-create our neighbours and live with an intention to thrive. Turn our backs on this hamster wheel and give yourself permission to be your greatest self.