Australian Housing Culture Is Incompatible With Rapid Urbanisation

Pouring the savings of an entire nation into the housing market creates destructive effects at the macro scale that make our cities worse today and unliveable tomorrow.

To make a rather tired point, the Australian economy is entirely too reliant on the housing market. About half of Australian household wealth is tied up in the value of the home, accounting for an average $509,000 out of a total average household assets of $1.1 million, despite one-third of householders not being home owners. On top of that, more than 20% of Australian households have an investment property or a holiday home, while only 10% of households own a business.

Australians have enjoyed decades of luxurious complacency when it comes to growing our wealth. Rather than explore diversified ways of funding retirement, we take on surreal amounts of debt with full confidence that someone in the future will borrow considerably more than we did. On top of paying a mortgage, we pour every spare cent into renovating our homes. Like spending a year in London or wearing open-toed footwear; it's just what we do - it doesn't really go deeper than that. Property is our national fetish. We are a nation of renovators. Scott Cam is our Warren Buffet.

"And what's wrong with that?" I hear your muffled voice call out from somewhere deep inside your recently-extended 6-bedroom inner-city cottage-slash-palace. "It's what our parents did and it worked out for them". It sure did - and good for them, but in the context of rapid urbanisation, pouring all of our money into housing creates destructive effects at the macro scale that make our cities worse today and unliveable tomorrow.

To own and renovate a home is to be Australian

To the typical Australian, our collective sense of accomplishment, stability and security is inseparable from home ownership. While all human beings understandably want the freedom to paint a wall, put up some pictures and get a horse-sized dog without having to prostrate yourself before a landlord, this idea of crippling amounts of debt being the one-and-only road to security and stability is a very Australian psychopathy.

It's that coming-of-age feeling when you playfully dab paint on your new bride's nose, while you convert a decrepit hovel into a white-on-white Hampstons-style Instagram post. It's that pang of confusion you feel when you meet a Baby Boomer who only owns one house. It's that tribal enmity you feel towards the ugly new townhouse development down the road. It's that swell of confidence you feel when you recite our national motto: "Rent money is dead money; property always goes up". These are all deeply-ingrained cultural narratives - constructs and clichés that feel natural, even human to us. But they are not the norm around the world.

The Swiss do it differently

In Switzerland, home ownership is the lowest in the OECD at roughly 40%, compared with an increasingly-decreasing 67% in Australia. Instead of subsidising unsustainable housing bubbles, the Swiss Government offers humane conditions for renters. The Swiss can get a long term lease. They can put up a picture. They can get a horse-sized dog. And most importantly, the Swiss do not stigmatise renting.

The opportunity cost of mass indebtedness is so large, it’s unknowable

If you think about it for more than five seconds, there is of course nothing secure or stable about owing a million dollars (plus interest). Tragically, the opposite is true. Due to the Kafkaesque, vampire-ridden process of buying and selling real estate, storing all of our wealth amidst iron-clad mortgage contracts makes us significantly less free, secure and stable. Indeed it seems self-evident that mortgages make us less likely to risk a new job or change careers, less able to start a side hustle, less likely to innovate, less likely to have children and less likely to take care of our own children. What would Australia even look like without this weight on our back? Mortgage debt is so intertwined with our culture, it’s difficult to imagine who and what we’d be without it.

Houses don't do anything

Despite the fact that houses have historically gone up in value, they don't actually do a whole lot in terms of economic activity. Characteristically, a house is closer to a bar of gold than it is to say, a factory. While a factory has the same type of "Dirt + (Bricks x Mortar) = Good" value that a house does - unlike housing, it also enables a process that actually creates economic activity and jobs over time. The humble house just sits there, relying on scarcity and society's perception of its value to accumulate, like gold.

No, I haven't forgotten about the unloved yoga studio in your garage - this is just to say that in comparison to a business, housing is a stagnant asset. Now zoom out and think about how much of the country's wealth is locked up in these unproductive assets, when it could be creating economic activity, jobs and innovation. This game of musical chairs we call the property market only creates new real estate agents and new seasons of The Block.

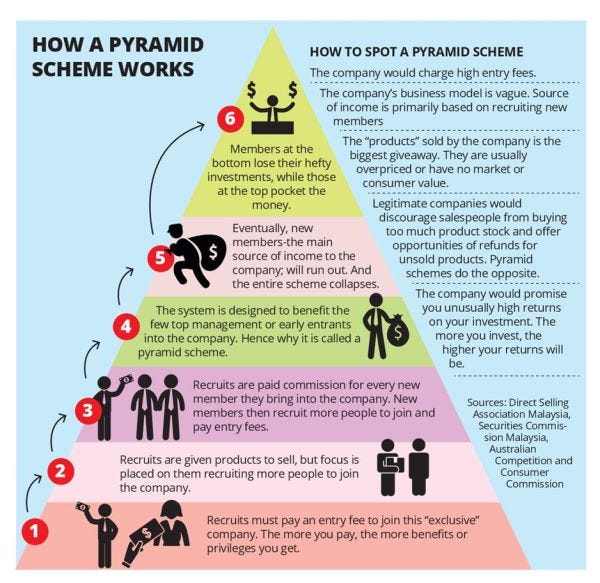

Australia is a pyramid scheme

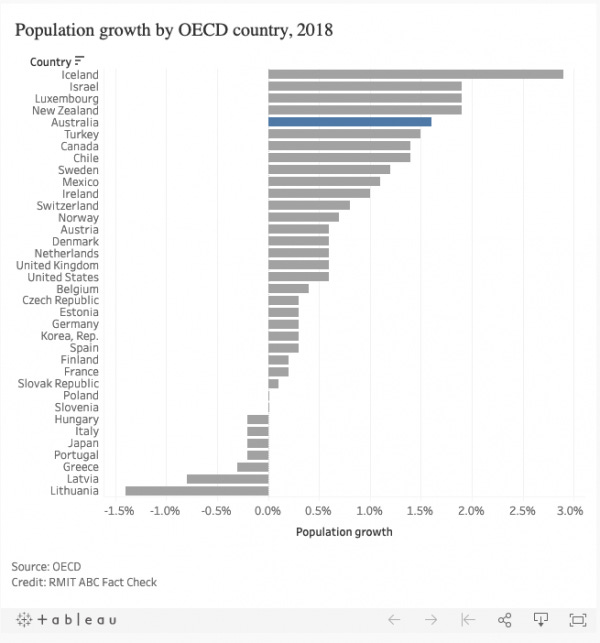

Aside from mining, Australia has a peculiar economy where we don’t really sell stuff to the world (like China does, for example). As a country, we’re less like a highly-productive factory and more like an exclusive country club with exorbitant membership fees. This is to say that a significant proportion of our growth comes from… growth. We simultaneously have low birth rates and the fifth highest population growth in the OECD due to high levels of net migration. A lot of the activity driving demand in our economy, comes from the fact that people want to live here. So one of the ways Australia stays rich is by recruiting new members. If this sounds a bit like Amway, that’s because it’s exactly like Amway.

{kind=link}

We are not managing rapid urbanisation well

Where this all starts to hit the rocks is when it meets the reality and scale of large cities. Australia is one of the world's most-urbanised populations, with 86% of Australians already living in cities. If for the foreseeable future, our prosperity is to be derived from flooding our cities with people to drive demand, we at the very least need to manage that growth in a way that preserves Australia's desirability as a place to live.

The bad news is we are not managing rapid urbanisation well at all, with overcrowded outer suburbs absorbing the brunt of low-cost housing, combined with shortfalls in public infrastructure like rapid transit and schools. Much like an exclusive country club limiting the number of available memberships, our cities are encumbered by layer after layer of regressive policies and structural flaws that hamstring our ability to meet this demand for housing and infrastructure in a way that actually protects what makes our cities great.

It all comes together in the perfect storm

Because of high levels of net migration, perpetually-low interest rates and the government generally propping up the property market wherever possible, demand for housing stays consistently-high. Because we are Australians, it is our life's purpose to make each of our many investment properties as expensive as humanly possible, instead of letting inner and middle suburbs organically renew into higher density typologies. Because NIMBYs are financially incentivised to pull up the drawbridge on Missing Middle development, local politicians are politically incentivised to make it impossible to build lower-cost housing in the inner and middle suburbs. A perfect storm of artificial scarcity, the cost of housing and infill renewal is driven higher and higher, while the path of least resistance guides new low-cost development into the outer fringes. Issues of income, race and housing affordability overlap considerably with one another, creating the added bonus of balkanising suburbs on racial and economic lines and burdening the poorest among us with longest, most-expensive commutes - effectively taxing the working class for not being rich. These are the unholy forces aligned to maintain Australia's endless property value growth at any and all cost.

The Australian lifestyle is at stake

There will be no clear tipping point where it becomes obvious to all that this paradigm is unsustainable. It will instead be a much more-insidious boiling of the frog over generations, as we acclimatise to a less-Australian (worse) quality of life. Just as we got used to living with COVID-19, we will simply teach ourselves to live with more vulnerability, less disposable income, longer commutes, endless traffic, shortfalls in infrastructure, homogenised wealthy inner city enclaves with racially and overcrowded, economically-segregated outer suburbs, all under the malaise of worsening inequality and environmental destruction. Not fun!

For what it's worth

If you have detected a not-so-subtle undercurrent of rage and frustration in my tone, it's probably because I myself fell victim to these incentive structures. Being a typical avocado-guzzling millennial knowledge worker, I loved living close to work and near all the cool restaurants and bars. I wasn't dying to go back to the 'burbs and spend hours of every week commuting, but I also wanted to put up some artwork and get a pet without naming our first child after our landlord. As one of Brisbane's many non-lawyers, houses close to the city were out of our price range. What about a unit? Alas - in Brisbane, units don’t hold value like houses do. I didn’t want to pour all that money into something that wasn't the best possible investment, so in the end, with all my spicy YIMBY opinions, my inner city cosmopolitanism and my deep concern about macroeconomic issues - I still ended up doing exactly what everybody else does - I bought a house that I could afford in the outer suburbs.

This says a lot about how powerful the cultural and financial incentives that undergird our economy are. Simply knowing about other ways of investing and growing wealth is still not enough to entice people away from home ownership, because our current conception of renting doesn't resonate to Australians as a life lived well.

Don’t hate the player, hate the game.

Coming Soon: What Is To Be Done

I appreciate that this article ended on a real down-note, but I am painfully aware that in the Current Year, it is unreasonable to expect people on the Internet to read too many words. I have set myself the goal of writing a series of policy proposals in a follow up article, so I don't come off as a complete doomsayer - even though that is my specialty.

UPDATE

My follow up article: How to solve housing un(affordability) - Part 1 - Legalise “The Missing Middle” is now posted.

In the mean time... subscribe to my Substack!

Over the holiday break I went through a bout of "New Year, New Me" hysteria and decided to start publishing my articles on Substack. I really like Substack, because when you are subscribed, you are able to read my full articles (complete with images) in your email inbox - sparing you having to go to the actual website or be lucky enough to spot my articles in your feed. For whatever reason I find this a much more enjoyable and consistent way to read the writers I follow, so if you have enjoyed any of my articles so far, please subscribe. Obviously, it is completely free.

I just discovered your site, so first off, I love it and am happily subscribed and reading more!!

This one struck a particular nerve with me because I was reading through a particularly frustrating (but not unsurprising) thread on Reddit where the unpopular opinion was that they liked renting more than buying. The comments were 70% "you're an idiot a home is an investment you're throwing your money away" and 25% doom of a generation priced out, and the tiny remainder talking sense, that in many circumstances this is true. Financial arguments were good there (index fund with better returns, not considering full costs, etc). But it was frustrating to see this just completely missed by most. The pressure that is put on by everyone around you that anything other than buying a home means you are a failure and will die in poverty, is just perpetuating this cycle and making it worse for everyone. I'm not sure if the analogy works, but it's perhaps like how everyone here (US) must have a car payment and drive a $50k truck - because you're at worse a loser and at best putting your family's lives at risk if you do anything less.

Regardless, you said it far better than I, but I just wanted to say I appreciate it all!!

Hey Riley love you article and insight on the housing market in Australia. Perhaps there is a path that can deliver the missing middle within this chaos otherwise known as the Australian housing market.